Ver en Español

It may look like TitleMax is just in the business of loans on car titles. But for us, it’s much deeper than that. We’re in the business of helping people. Whether that’s through our all-credit-welcome policy, our fast approval process, or our quick turnaround time, our goal is to help you get the cash you need right when you need it most. Our customers mean a lot to us, and we firmly believe that we only succeed when you succeed. That’s why we spend ample time and attention training each and every one of our TitleMax team members. To us, it’s about much more than just auto title loans: It’s about giving you the options you need to take care of your finances.

We’re Here for You with Same-Day in Store Title-Secured Loans/Pawns or Personal Loans

When you visit us in store, you’ll find that our customer service representatives have the tools and knowledge to help you decide if a title or personal (where applicable) product is best for you. Our focus on your convenience is also why we have more than a thousand locations nation-wide, and why we let you keep driving your car throughout while you pay off your loan/pawn. It’s also why we work with you from start to finish with explanations and walkthroughs of the process. From an easy-to-use Customer Portal and convenient store locations, to a robust text message reminder program to help you stay on track, we have designed our business around you.

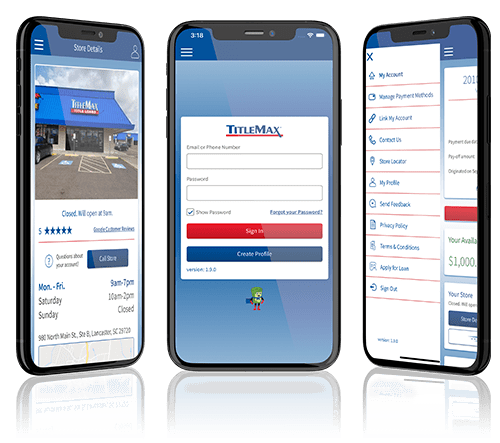

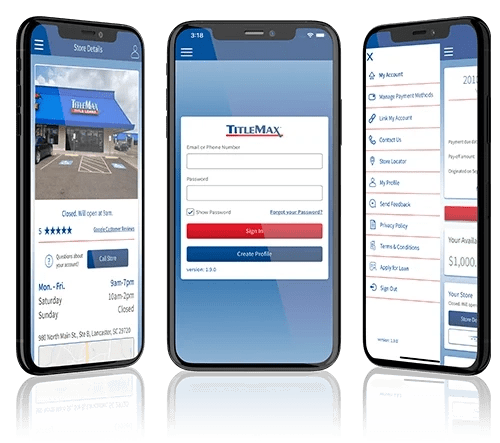

Click & Mortar™ Gives You Even More Flexibility

Payments and account servicing have never been easier for TitleMax customers. You’ve always had the option of returning to your store to speak with an associate for assistance, and now through the TitleMax Customer Portal, you can manage your account with us right through your mobile phone or desktop.

Types of TitleMax Loans

Borrowers can choose a number of TitleMax title loan options, depending on their needs and situation. TitleMax offers:

Car Title Loans

Car Title Pawns

Motorcycle Title Loans and Pawns

Personal Loans

At TitleMax, we believe that past downfalls should not determine the rest of your life. Each and every step we take with our car title loans is aimed at ensuring your complete satisfaction with us and the ultimate success of your future. Benefit from our all-credit-welcome policy and let us help you get your finances back on track!

TitleMax Offers Numerous Loan Options

Car Title Loans/Pawns

A title loan is an easy way to get cash using your car title instead of your credit score. Your title loan size may be determined by the amount of cash you need, your vehicle’s value, and your ability to repay. TitleMax offers car title loans up to $10,000*, and we focus on getting you the most cash possible while keeping your payments manageable. If you have a title loan with another company, we’ll pay it off and cut your rate in the process.§ We make it easy to get the title loans you need with reliable service.

TitleMax offers car title pawns in its Georgia stores. Similar to a car title loan, a title pawn is a simple way to get cash fast using your vehicle as collateral. If you have a clear car title and a government-issued ID, you can get a title pawn with TitleMax even if you have bad credit. Already have a title pawn with someone else? Switch to TitleMax! In most cases, we can lower the rate on your existing pawn and pay off your current loan.

A motorcycle title loan is a great way to get cash in as little as 30 minutes by using your title. The amount of cash you’re approved for depends on satisfaction of all loan eligibility requirements including your motorcycle’s value, your cash need, and a credit evaluation. At TitleMax, we also work to get you as much cash as we can at very competitive rates.

In our Georgia TitleMax stores, we offer motorcycle title pawns and any credit is welcomed. A motorcycle title pawn is just like a car title pawn in that they are all fast and easy ways to get cash by using a vehicle as your collateral.

TitleMax in-store and online personal loans and lines of credit offer a quick application process and they differ from title-secured loans/pawns because they are unsecured loans, meaning that you can apply for one even if you do not own a vehicle with a clear title. To get a personal loan you can get started online by reviewing the requirements and head in to one of our designated TitleMax stores, or you can skip the visit and apply for an online personal loan from the comfort of your own home! We can have you on your way to getting your life back on track in as little as 30 minutes in-store, or as soon as the next business day online.